-

Let’s Make Critical Mineral Lists More Useful!

In December 2024, China banned exports of gallium, germanium, and antimony to the United States. Prices for these critical minerals soon reached all-time highs. The ban emphasized China’s dominance over the sector, including practically the entire graphite supply chain, 87% of rare earths refining, 70% of cobalt refining, and 60% of battery-grade lithium refining.

And when trade tensions with the United States escalated in February 2025? China again expanded controls over key critical minerals exports.

The growing awareness of China’s dominance over critical minerals processing and refining has led at least 20 countries to create critical mineral lists. They indicate each country’s investment priorities for diversifying supply or onshoring value-added processes. Yet over the last decade, these critical mineral lists have not stopped China’s dominance over critical mineral refining and processing.

How can they be made more effective? Countries should restructure their critical mineral lists and pair them with clear fiscal and regulatory incentives. Achieving clarity in goals and support would aid private investor efforts to move critical mineral-related manufacturing out of China.

What Makes a Mineral Critical?

Making critical mineral lists more useful might begin with countries placing themselves within what is known as the “stable marriage problem”: two classes of actors seek to match with each other and achieve a stable outcome when no actor prefers another match to the one it has. (This process is how matching medical students to residencies works in the United States, for instance.)

This technique also might create more balanced critical mineral supply chains. Yet getting to that point requires a clear understanding of what critical minerals are.

Twenty years ago, the only list of critical minerals—created by Spain—included ornamental rocks, talcum powder, and coal. The importance of critical minerals in our own moment is often tied to green energy technology like solar panels and EV batteries. Indeed, critical minerals are often defined by international bodies as “energy transition minerals.”

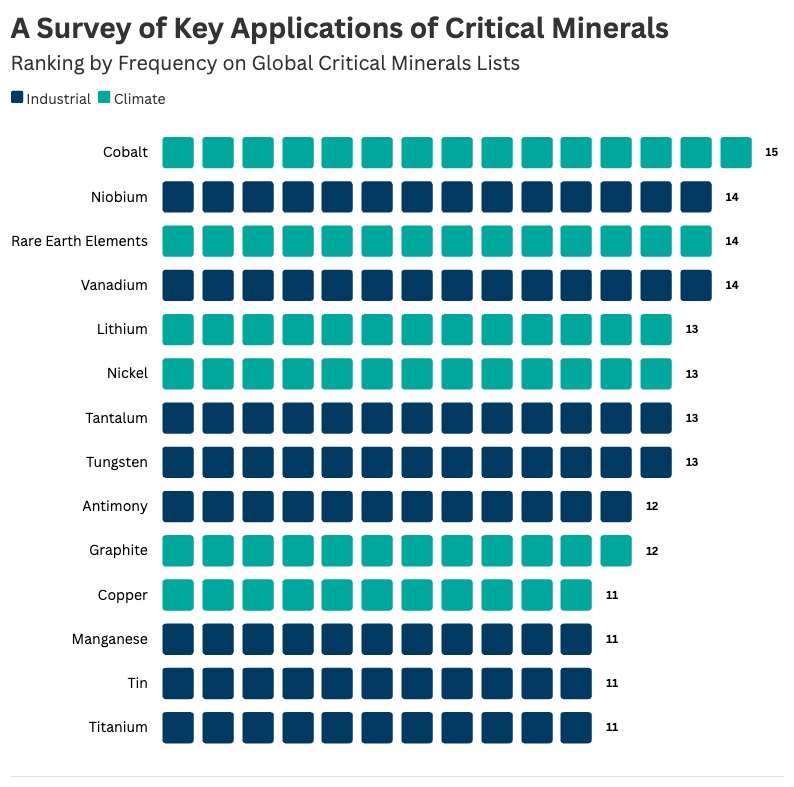

But our own recent survey of 20 lists, comprised of ten from developed countries (including the European Union) and ten from developing countries (including China), paints a more complicated picture. Fourteen minerals appear on more than half of critical mineral lists, but only 6 see significant end-use in clean energy and climate-related sectors. (See Infographic 1). The remainder are reserved for industrial purposes. Germanium, which is at the center of the recent US-China dispute, does not even make this list—and it’s not used primarily for clean energy purposes.

Infographic 1. Critical Mineral Lists-Common Minerals and Uses

Countries determine whether a mineral is critical using formulas that consider factors including domestic economic importance, global demand, and supply chain risk (with import reliance often used as a gauge). Strategic relevance and substitutability are also considered. Whether other countries consider including it on their lists of other countries also carries weight.

Some lists—notably those of Canada and the EU—do factor in a mineral’s importance to the green transition. Yet the net effect is to make critical mineral lists tools to identify areas of Chinese dominance, and not to lay out steps on the path to decarbonization.

Because many critical mineral lists are recent creations, it can be hard to assess their effects. Early signs are not encouraging, however. Only seven lists are accompanied by frameworks for public investment in critical mineral mining and refineries. And despite significant incentives (such as the United States’ Inflation Reduction Act), low critical mineral prices have made it a challenge to translate intentions into increased mineral production. In fact, most critical mineral lists do not lean into assessing comparative advantages in mineral extraction or processing, nor are they accompanied by legal reforms that would de-risk investment. They also lack fiscal incentives to make downstream processing, refining, and manufacturing competitive with China.

These gaps mean that developed countries have struggled both to find suppliers of refined commodities such as graphite and cobalt outside China and expand their own domestic downstream processing. Developing countries languish upstream, confined to extractive processes and unable to tap into the more lucrative opportunities of processing, refining, and manufacturing associated with critical minerals.

Charting a Future for Critical Mineral Lists

This situation can be changed. If countries restructure their lists to map out how they will address their critical mineral vulnerabilities, they could play a key role in creating more balanced supply chains that meet the needs of developed and developing countries—providing less industry concentration and more economic security.

Indonesia is home to the world’s largest nickel reserves. It is one country that has successfully executed a transition from extraction to downstream processing. For years, Chinese mining operations exported raw nickel back to China for processing. But in 2020, the Indonesian government banned nickel ore exports in a bid to onshore nickel refining.

Chinese nickel refiners proved willing to move production to Indonesia. The change was marked: Indonesia’s share of global refined nickel production stood at 23% in 2020—and rose to 37% in 2024. It is projected to reach 44% by 2030.

While Indonesia’s ban was not associated with a critical minerals list, the effective use of a “stick” offers an example for how countries can think about securing matches for investment and onshoring. Thailand’s success at localizing EV production by attracting investment from Chinese firms provides another good template.

China’s pivotal role in efforts to localize supply chains is clear. To avoid continuing critical minerals concentration, other countries should decide if mineral extraction or onshore value-added processes are a priority. Some country lists already envision this shift, but more can be done to make this divide clearer to facilitate more targeted fiscal and policy incentives.

Imagine Country A as a significant producer of copper ore which has struggled to onshore processing and refining of the raw material. Its critical minerals list might indicate a willingness to offer favorable factory sites and tax credits for investments in copper refining joint ventures and outline a plan to raise export barriers. Country B’s list may express interest in diversifying its sources of refined copper beyond China and offer concessional loans to refining ventures in third countries. Country A and Country B would have an ideal match facilitated by effective use of critical mineral lists.

The last stage for countries with restructured lists is to catalyze such matches. This could happen bilaterally, or within a forum like the Minerals Security Partnership. In the equilibrium outcome, each country would sign agreements that it prefers to any other option.

Critical mineral lists are not tools of the energy transition. They are tools of geopolitical competition with the potential to rectify imbalances in global development and industrial supply chains. To fulfill that potential, countries need to reconsider the kinds of information they provide in their critical mineral lists and how they use them to communicate preferences and objectives. Our template provides one way of doing that.

Daevan Mangalmurti is a junior fellow at the Carnegie Endowment for International Peace

Debbra Goh is a junior fellow at the Carnegie Endowment for International Peace

Sources: Australia Critical Minerals Strategy, Brazil Official Press Release, Economic Times, Energyworld, Energy Mix, European Commission, European Union, Geoscience Australia, Government of Canada, India Industry of Mines, International Energy Agency, Spain Official Press Release, Statista, The Energy Mix, Mining Technology, Reuters, S&P Global, UN Conference on Trade and Development, UC Davis Institute of Transportation Studies, US Department of the Interior Geological Survey, US Department of State

Photo credit: Ge (Germanium) Ga (Gallium) in the periodic table with Chinese flag. US vs China chip war or tech war, microchip semiconductor industry concept. China curbs on exports of rare germanium and gallium. Photo courtesy of Shutterstock / Pla2na

Figure credit: Courtesy of authors

A Publication of the Stimson Center.

A Publication of the Stimson Center.