-

More than Just a BRI Greenwash: Green Bonds Pushing Climate-Friendly Investment

December 13, 2018 By Alan Meng

From the cultural hub of Lahore down to the bustling ports of Karachi, smog is king in Pakistan, with citizens enduring unhealthy air quality for much of the year. The smog, generated mostly by crop and garbage burning and diesel emissions from furnaces and cars, could get worse by the end of this year when Pakistan opens five new Chinese-built coal power plants, funded by a $6.8 billion venture under the China-Pakistan Economic Corridor (CPEC) initiative. These five plants are just the beginning of the Pakistan government’s planned 7,560 MW expansion in coal power, which are CPEC-energy priority projects. “It’s a perfect storm for a pollution crisis,” said Michael Kugelman of the Wilson Center’s Asia Program. “The poor will continue to burn a variety of polluting materials to produce fuel, and now you’re also going to be introducing dirty coal into the mix. Combine that with crop burning in the countrywide and car exhaust fumes in rapidly growing cities, and you’ve got a really smoggy mess on your hands—and in your lungs.”

Pakistan is not the only recipient of Chinese fossil fuel investments. Under China’s Belt and Road Initiative (BRI), Chinese banks, companies, and investors are pouring money into coal, wind, and solar power projects, as well as connectivity infrastructure, such as high-speed rail, expressways, and ports. Energy receives the lion’s share of investment across many of the 69 BRI member countries, with coal and oil making up nearly 60%. These energy projects will deliver much needed electricity, but at a cost. 6 out of the 10 most climate change vulnerable countries in the world are in BRI’s ambit. Xi Jinping has called for a Green BRI, but with such a high percentage of the investments in black energy, Chinese banks, companies, and investors need to wield new green finance tools if they hope to promote truly greener infrastructure.

Growth of the Global Green Bond

According to the Climate Bonds Initiative and other financial analysts, green bonds will likely be one of the prominent channels to mobilise private capital efficiently while making the investment green in BRI countries. Despite controversy over greenwashing bonds, China seeks to mobilize and streamline green bonds, working with its own national banks and other international investment players.

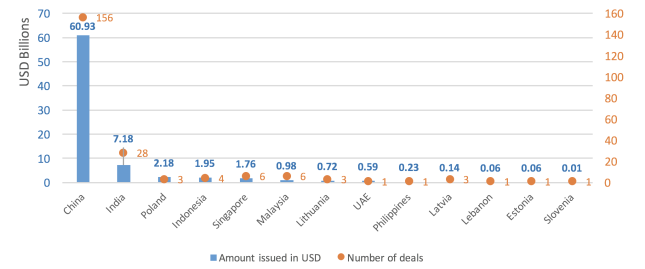

Since 2007, the European Investment Bank and the World Bank launched the green bond market as a mechanism to fund climate-change related finances. More than 10 years later, the global green bond market has grown leaps and bounds, with a market size standing around $463 billion. According to the Climate Bonds Initiative, renewable energy and low carbon transport constitute 58% of the total proceeds allocation.

In China alone, the People’s Bank of China (PBoC) became one of the largest influencers in green finance; in the past two years, China’s green bond market expanded to become one of the world’s largest. The rapid growth sent aftershocks from the national level down to the provincial. Following a record-breaking year in 2016, China’s green bond market cultivated a growing momentum at the local level driven by regional commercial banks and local government financing vehicles. By the end of Q3 2018, China became the second largest source for green bonds, a market totalling $61 billion.

Asia requires up to $900 billion of infrastructure investment per year within the next 10 years, indicating a major opportunity for BRI green infrastructure projects. Green initiatives such as wind farms, national passenger high-speed railway, urban mass transit, and building resiliency infrastructure, intrinsically have low carbon features and are well-suited with green financing infrastructure via debt instruments.

Green BRI Not Only a China Project

China’s international collaborations with European markets, such as Luxembourg, London, Dublin, and Euronext, are creating opportunities for funding green BRI infrastructure bonds. In October 2017, the Industrial and Commercial Bank of China brought $2.14 billion Climate Bonds Certified green bonds through its Luxembourg branch, marking the first ever dedicated “Green Belt and Road Bond.” All the proceeds are expected to support projects in China’s domestic provinces and in other key BRI countries, such as offshore and onshore wind, solar, tidal, and hydropower, and low carbon transport such as rail tram, metro, bus rapid transit systems, and electric vehicles. In June 2018, Climate Bonds Certified green bonds followed with another $1.58 billion from its London branch, with proceeds financing low carbon projects such as multiple onshore wind and solar farms across different provinces in China and Pakistan, as well as a wind farm project in Scotland.

Despite Potential, Challenges Await

Despite the plethora of opportunities, green bond issuers and recipients in BRI countries face many challenges. In the short-term, one difficulty is to identify and standardize green project qualifications, while in the long-run, it will be challenging to increase financial infrastructure in favour of green bonds, and to attract more international investors. The development of green bond listing rules at stock exchanges and indices can expand and solidify green financial infrastructure. These rules combined with better standards for green qualifications will help wariness of projects that may be considered green in one context, and not in another. For example, retrofits of fossil fuel power stations, clean coal and coal efficiency improvements, and electricity grid transmission infrastructure carrying fossil fuel energy are permissible under China’s domestic green bond definitions; however, such guidelines are not in line with the expectations of international investors. As a critical step next, green bond issuance in BRI countries needs to be scaled up and diversified.

Lastly, strategic green bond demonstration issuance could encourage investors and educate them about asset classes. As a new catalyst to the green finance development, a greener BRI is expected to further accelerate the collaborations among BRI countries and encourage regional development banks, municipalities, national government and well-placed public-private partnerships. “When it comes to emphasizing more clean energy in Pakistan, the incentive structure is a bit out of whack,” said Kugelman. “Green bonds would be a very helpful motivating factor for getting more clean energy investment into Pakistan. And they could go a long way toward helping make the air a bit cleaner.”

Alan Xiangrui Meng is a green bond analyst based in Climate Bonds Initiative’s London office. He leads the data analysis on China’s green bond market, maintains and updates China Climate-aligned Bond Index, and provides research on China’s green finance policies. He is a member of the UN Sustainable Stock Exchange Initiative’s Green Finance Advisory Group.

Sources: Beatrice Offshore Windfarm Ltd., Boston University Global Development Policy Center, China Pakistan Economic Corridor, Chinese Government, Climate Bonds Initiative, Euronext, Institute for Energy Economics and Financial Analysis, Quartz, Verisk Maplecroft, World Bank

A Publication of the Stimson Center.

A Publication of the Stimson Center.